June 2, 2026

Navigate LOE with confidence

Loss of exclusivity doesn’t have to mean losing stakeholder engagement. Discover how BaseCase helps communicate differentiated value through interactive, omni-channel experiences that support payers, providers, and patients throughout the LOE transition.

Key challenges driven by loss of exclusivity in pharma

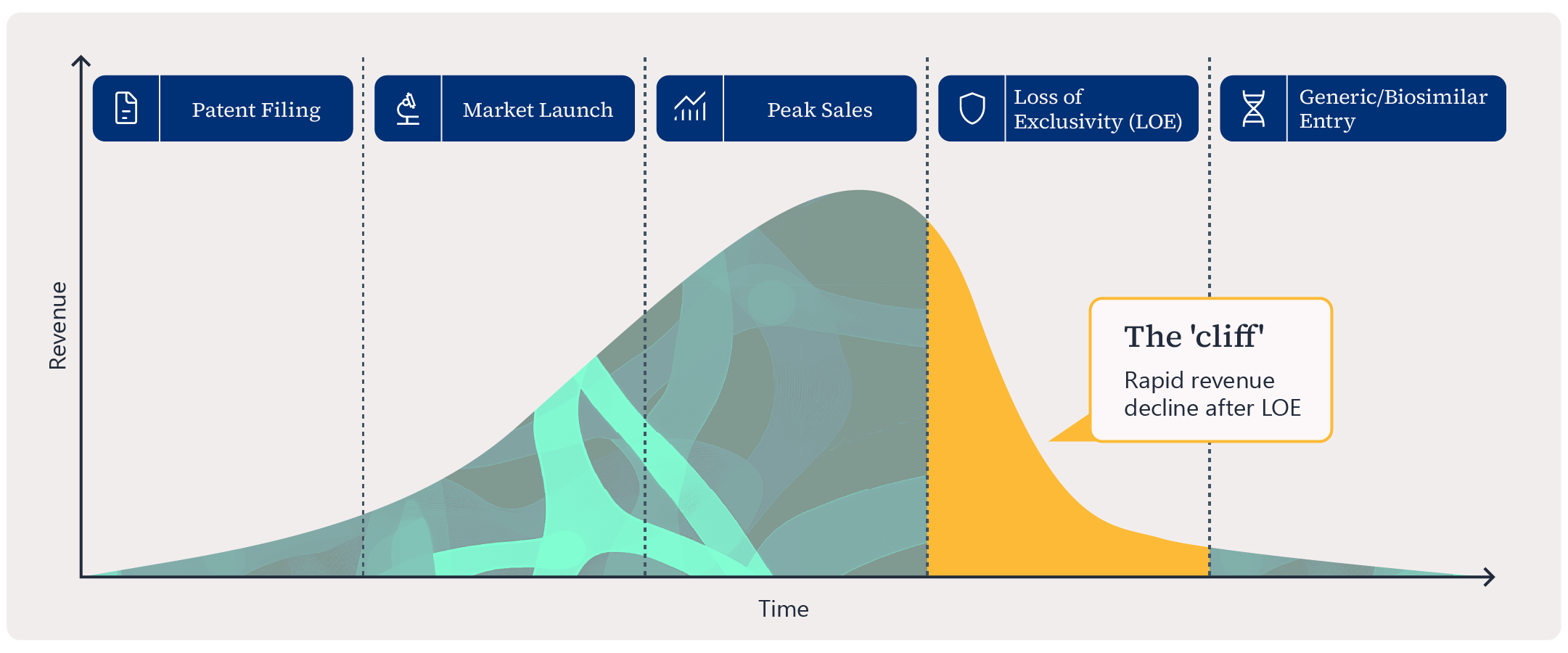

1. Revenue erosion

Steep declines as generics and biosimilars enter the market

2. Increased competition

More competitors intensify pricing pressure and margin erosion

3. Market share decline

Generics capture significant share soon after launch

4. Complex supply chains

Biologics require sophisticated manufacturing and cold-chain logistics

5. Specialized markets

Niche therapies serve smaller populations requiring tailored approaches

6. AI-driven 'me-too' proliferation

Fast-follower therapies intensify fragmentation and competition

Integrated execution across these strategies helps maintain patient access, strengthen stakeholder trust, and protect revenue beyond loss of exclusivity.

Defend market share beyond LOE

As competition intensifies post-LOE, delivering consistent, value-driven messaging becomes critical. Explore how BaseCase enables pharma teams to turn complex evidence and market access content into interactive tools that engage payers, providers, and decision makers.

This blog was originally published on October 21, 2024 and has been updated for accuracy.

Christian Pichardo

Director, Product ManagementChristian Pichardo serves as Director of Product Management at Certara/BaseCase. He leads the design and strategic direction of digital solutions that strengthen health economics and value communication, ensuring alignment with customer needs and market trends.

Before stepping into his current role, Mr. Pichardo spent more than 15 years working across the life sciences, consulting, and software industries, holding leadership roles in market access, health economics, and product strategy. In addition to his corporate experience, he has co-founded consulting ventures focused on healthcare innovation and capability development, further broadening his perspective on advancing access and value in healthcare.

Mr. Pichardo holds degrees in Economics and Applied Mathematics from the Instituto Tecnológico Autónomo de México (ITAM) and a Professional Certificate in Product Management from the Massachusetts Institute of Technology (MIT). He has published peer-reviewed research on cost-effectiveness and real-world outcomes in leading scientific journals.

Make an inquiry

Navigate loss of exclusivity with more effective value communication. See how BaseCase helps pharma teams deliver interactive, omni-channel stakeholder engagement before and after LOE.

Communicate differentiated product value

Support payer and market access conversations

Deliver interactive evidence and economic models

Maintain compliant messaging across channels

FAQs

How can pharmaceutical companies prepare for loss of exclusivity (LOE)?

Pharmaceutical companies can prepare for loss of exclusivity by implementing a proactive lifecycle management plan years before patent expiry. Effective approaches include launching improved formulations, pursuing new indications, strengthening payer relationships, and using omnichannel engagement to reinforce product value. A strong loss of exclusivity strategy also helps companies reduce the commercial impact of generic or biosimilar competition.

What are the most effective pharmaceutical patent strategies before LOE?

Successful pharmaceutical patent strategies often focus on extending product value before LOE occurs. Common approaches include obtaining additional exclusivity protections, developing combination therapies, introducing new delivery methods, and supporting differentiated clinical evidence. Many organizations also implement a broader patent cliff strategy that combines commercial, regulatory, and digital engagement tactics to sustain stakeholder confidence.

How can companies maintain market share after loss of exclusivity in pharma?

Maintaining market share after loss of exclusivity pharma events requires companies to differentiate beyond price alone. Successful approaches include patient support programs, value-based messaging, branded generics, and stronger payer engagement. A well-executed loss of exclusivity strategy also focuses on personalized stakeholder communication and consistent omnichannel engagement to reinforce product value in increasingly competitive markets. Learn how the BaseCase interactive platform can strengthen your value story before and after LOE.

Why is the pharmaceutical patent cliff such a major challenge for pharma companies?

The pharmaceutical patent cliff creates a sudden decline in revenue when multiple high-value drugs lose exclusivity at the same time. In loss of exclusivity pharma markets, companies often face rapid generic erosion, pricing pressure, and reduced market share within months of patent expiration. The challenge is especially significant for blockbuster therapies that previously generated large portions of company revenue.

What makes a successful patent cliff strategy in today’s pharmaceutical market?

A modern patent cliff strategy goes beyond defending revenue alone. Companies increasingly rely on omnichannel communication, real-world evidence, payer engagement, and personalized digital experiences to maintain product value after exclusivity ends. In today’s competitive loss of exclusivity pharma environment, successful strategies combine commercial execution with data-driven stakeholder engagement to preserve long-term market relevance. Watch the webinar to learn omni-channel strategies for loss of exclusivity: https://www.certara.com/on-demand-webinar/navigating-the-patent-cliff-omni-channel-strategies-for-loss-of-exclusivity-and-established-products/